The pandemic has hit server sales as enterprises held back and SMBs moved to the cloud. IDC's EMEA Server Tracker shows that in 2Q20 the EMEA server market reported a year-on-year decrease in vendor revenues of 5.8% to $3.9 billion and a yr/yr decrease of 6.9% in units shipped to around 470,000.

When viewing the EMEA market by product detail, the impact of COVID-19 can clearly be seen, as the SMB market has both seen a slowdown in run rate business and faster adoption of cloud platforms. Tower shipments in 2Q20 decreased 32.5% QoQ, while custom shipments targeted toward cloud platforms grew 8.9% QoQ. Lenovo continued to penetrate the hyperscale market and saw significant growth in 2Q20, it says.

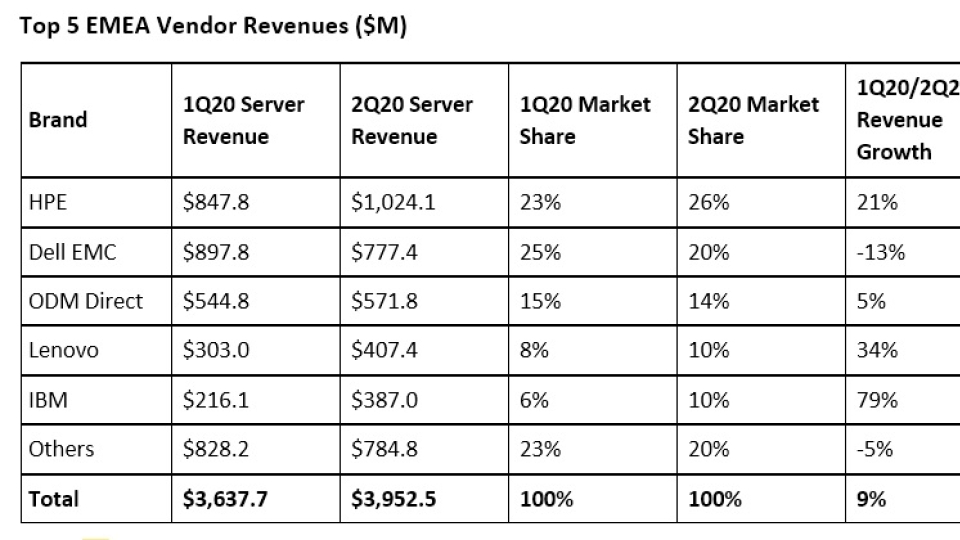

Vendor performance is shown in the table: Dell saw a fall in market share, with HPE and IBM picking up numbers.

"This strong growth in ASPs is a result of both a shift toward higher socket counts and richer configuration component configurations as the market grapples with digital transformation to ensure business continues in these trying times," said Eckhardt Fischer, senior research analyst in the European Infrastructure group.

"ODM shipments are back to pre-COVID levels worldwide and ODM manufacturing facilities are reporting 24 x 7 activity to close the gap in production caused by anti-COVID measures earlier this year and meet COVID-related demand for cloud-deployed digital services," said Kamil Gregor, senior research analyst in the European Infrastructure group. "In the short term, it seems that a 1Q20 drop in consumption has been overcome, but we still need to wait for the longer-term impact of the economic slowdown on infrastructure vendors and buyers and consumers of digital services."

Looking at the Western European x86 server market, the UK performed well, growing 11.8% YoY in revenue, driven by hyperscale datacenter investments. The same trend was seen in the Netherlands and Ireland in 2Q20. With around $660 million in revenue, Germany maintained its position as the region's largest market.

"Central and Eastern Europe, the Middle East, and Africa [CEMA] server revenue continued its downward trajectory in 2Q20, declining 5.9% year over year to $791.31 million," said Jiri Helebrand, research manager, IDC CEMA. "Reduced business activity due to COVID-19 was the main reason for weak sales, although there are strong differences in performance across the region. The Central and Eastern Europe [CEE] subregion grew 6.9% year over year with revenue of $424.83 million. Ukraine, Czech Republic, and Russia recorded the strongest growth. Cloud platforms, online services, and strengthening infrastructure to support working from home helped drive sales. The Middle East and Africa [MEA] subregion declined 17.3% year over year to $366.48 million in 2Q as some IT projects were put on hold and nationwide lockdowns and a reduction in cargo flights in some parts of the African region had a negative impact. Israel and Bahrain were the only countries in MEA to record growth."